The term gambler's ruin is used for a number of related statistical ideas:

The ideas have specific relevance for gamblers; however they are also general theorems with wide application and many related results in probability and statistics. Huygens' result in particular led to important advances in the mathematical theory of probability.

The earliest known mention of the gambler's ruin problem is a letter from Blaise Pascal to Pierre Fermat in 1656 (two years after the more famous correspondence on the problem of points). Pascal's version was summarized in a 1656 letter from Pierre de Carcavi to Huygens:

Let two men play with three dice, the first player scoring a point whenever 11 is thrown, and the second whenever 14 is thrown. But instead of the points accumulating in the ordinary way, let a point be added to a player's score only if his opponent's score is nil, but otherwise let it be subtracted from his opponent's score. It is as if opposing points form pairs, and annihilate each other, so that the trailing player always has zero points. The winner is the first to reach twelve points; what are the relative chances of each player winning?

Huygens reformulated the problem and published it in De ratiociniis in ludo aleae ("On Reasoning in Games of Chance", 1657):

Problem (2-1) Each player starts with 12 points, and a successful roll of the three dice for a player (getting an 11 for the first player or a 14 for the second) adds one to that player's score and subtracts one from the other player's score; the loser of the game is the first to reach zero points. What is the probability of victory for each player?

This is the classic gambler's ruin formulation: two players begin with fixed stakes, transferring points until one or the other is "ruined" by getting to zero points. However, the term "gambler's ruin" was not applied until many years later.

Let "Bankroll" be the amount of money a gambler has at his disposal at any moment, and let N be any positive integer. Suppose that he raises his stake to  when he wins, but does not reduce his stake when he loses. This general pattern is not uncommon among real gamblers, and casinos encourage it by "chipping up" winners (giving them higher denomination chips). Under this betting scheme, it will take at most N losing bets in a row to bankrupt him. If his probability of winning each bet is less than 1 (if it is 1, then he is no gambler), he will eventually lose N bets in a row, however big N is. It is not necessary that he follow the precise rule, just that he increase his bet fast enough as he wins. This is true even if the expected value of each bet is positive.

when he wins, but does not reduce his stake when he loses. This general pattern is not uncommon among real gamblers, and casinos encourage it by "chipping up" winners (giving them higher denomination chips). Under this betting scheme, it will take at most N losing bets in a row to bankrupt him. If his probability of winning each bet is less than 1 (if it is 1, then he is no gambler), he will eventually lose N bets in a row, however big N is. It is not necessary that he follow the precise rule, just that he increase his bet fast enough as he wins. This is true even if the expected value of each bet is positive.

The gambler playing a fair game (with 0.5 probability of winning) will eventually either go broke or double his wealth. These events are equally likely, or the game would not be fair (ignoring the fact that his bankroll might jump over one event or the other, this is a minor complication to the argument). So he has a 0.5 chance of going broke before doubling his money. Once he doubles his money, he again has a 0.5 chance of doubling his money before going broke. Overall, there is a 0.25 chance that he will go broke after doubling his money once, but before doubling it twice. Continuing this way, his chance of going broke is 0.5 + 0.25 + 0.125 + . . . which approaches 1.

Huygens' result is illustrated in the next section.

The eventual fate of a player at a negative expected value game cannot be better than the player at a fair game, so he will go broke as well.

Consider a coin-flipping game with two players where each player has a 50% chance of winning with each flip of the coin. After each flip of the coin the loser transfers one penny to the winner. The game ends when one player has all the pennies.

If there are no other limitations on the number of flips, the probability that the game will eventually end this way is almost surely 1. (One way to see this is as follows. Any given finite string of heads and tails will eventually be flipped with certainty: the probability of not seeing this string, while high at first, decays exponentially. In particular, the players would eventually flip a string of heads as long as the total number of pennies in play, by which time the game must have already ended.)

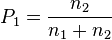

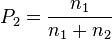

If player one has n1 pennies and player two n2 pennies, the probabilities P1 and P2 that players one and two, respectively, will end penniless are:

Two examples of this are if one player has more pennies than the other; and if both players have the same number of pennies. In the first case say player one  has 8 pennies and player two (

has 8 pennies and player two ( ) were to have 5 pennies then the probability of each losing is:

) were to have 5 pennies then the probability of each losing is:

= 0.3846 or 38.46%

= 0.3846 or 38.46%

= 0.6154 or 61.54%

= 0.6154 or 61.54%It follows that even with equal odds of winning the player that starts with fewer pennies is more likely to fail.

In the second case where both players have the same number of pennies (in this case 6) the likelihood of each losing is:

=

=  =

=  = 0.5

= 0.5 = = = 0.5

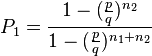

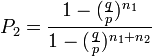

= = = 0.5In the event of an unfair coin, where player one wins each toss with probability p, and player two wins with probability q = 1-p, then the probability of each ending penniless is:

This can be shown as follows: Consider the probability of player 1 experiencing gamblers ruin having started with  amount of money,

amount of money,  . Then, using the Law of Total Probability, we have

. Then, using the Law of Total Probability, we have

,

,where W denotes the event that player 1 wins the first bet. Then clearly  and

and  . Also

. Also  is the probability that player 1 experiences gambler's ruin having started with

is the probability that player 1 experiences gambler's ruin having started with  amount of money:

amount of money:  ; and

; and  is the probability that player 1 experiences gambler's ruin having started with

is the probability that player 1 experiences gambler's ruin having started with  amount of money:

amount of money:  .

.

Denoting  , we get the linear homogeneous recurrence relation

, we get the linear homogeneous recurrence relation

,

,which we can solve using the fact that  (i.e. the probability of gambler's ruin given that player 1 starts with no money is 1), and

(i.e. the probability of gambler's ruin given that player 1 starts with no money is 1), and  (i.e. the probability of gambler's ruin given that player 1 starts with all the money is 0.) For a more detailed description of the method see e.g. Feller (1957).

(i.e. the probability of gambler's ruin given that player 1 starts with all the money is 0.) For a more detailed description of the method see e.g. Feller (1957).

The above described problem (2 players) is a special case of the so-called N-Player ruin problem. Here  players with initial capital

players with initial capital  dollars, respectively, play a sequence of (arbitrary) independent games and win and lose certain amounts of dollars from/to each other according to fixed rules. The sequence of games ends as soon as at least one player is ruined. Standard Markov chain methods can be applied to solve in principle this more general problem, but the computations quickly become prohibitive as soon as the number of players or their initial capital increase. For

dollars, respectively, play a sequence of (arbitrary) independent games and win and lose certain amounts of dollars from/to each other according to fixed rules. The sequence of games ends as soon as at least one player is ruined. Standard Markov chain methods can be applied to solve in principle this more general problem, but the computations quickly become prohibitive as soon as the number of players or their initial capital increase. For  and large initial capitals

and large initial capitals  the solution can be well approximated by using two-dimensional Brownian motion. (For

the solution can be well approximated by using two-dimensional Brownian motion. (For  this is not possible.) In practice the true problem is to find the solution for the typical cases of and limited initial capital. Swan (2006) proposed an algorithm based on Matrix-analytic methods (Folding algorithm for ruin problems) which significantly reduces the order of the computational task in such cases.

this is not possible.) In practice the true problem is to find the solution for the typical cases of and limited initial capital. Swan (2006) proposed an algorithm based on Matrix-analytic methods (Folding algorithm for ruin problems) which significantly reduces the order of the computational task in such cases.